Summary

- Curtiss-Wright Corporation has a strong fundamental outlook and potential for upside growth.

- The company reported strong revenue growth in Q4 2023, driven by performance in Commercial Aerospace and Defense markets.

- Curtiss-Wright’s profitability improved marginally in 2023, and its long-term earnings outlook is positive.

- Adjusted EPS growth and consistent shareholder returns indicate potential, but caution is advised due to current valuation.

Investment Thesis

Curtiss-Wright Corporation (NYSE: CW), in my view, is not a stock with huge upside potential at this price level, as it has already increased by around ~42% in the last year. The company looks well-positioned to continue benefiting from the strong backlog of $2.9 billion as well as robust demand across its end markets. It also provides the company with the opportunity to improve adjusted free cash flow and shareholder returns through share repurchases and potential dividend increases. The company is also expected to benefit from strong industry tailwinds like high defense spending worldwide and re-emerging trends for nuclear energy demand through its Generation III and Gen IV advanced (SMRs) design products.

Furthermore, with the acquisition of the arresting system in 2022, it has strengthened its position in Aerospace and Naval Defense markets. But at the current valuation, I have a neutral rating on the stock, beacause the strong industry tailwinds is getteing offset by slight overvaluation.

About the Company

Curtiss-Wright Corporation, based on its 10K 2023, “is a global integrated business that provides highly engineered products, solutions, and services mainly to Aerospace & Defense (A&D) markets, as well as critical technologies in demanding commercial power, process, and industrial markets.” They say they have an additional advantage over peers, especially during a high inflationary environment, that is its ability to offset negative impacts from inflationary pressure through lean manufacturing and passing high costs to its customers through price increases, which are possible due to specific terms in their contracts. This is evident from the fact that its adjusted operating margin for the year 2023 was at a record high of 17.4%.

Revenue Analysis And Outlook

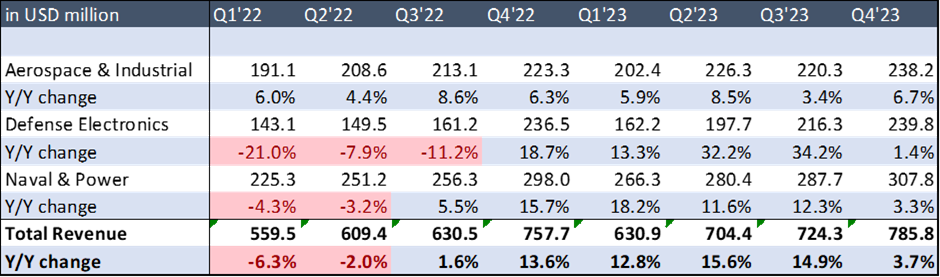

In the fourth quarter of 2023, Curtiss-Wright beat consensus estimates as it reported revenue of $785.8 million, an increase of over 3.7% YoY. This growth was driven by strong performance in Commercial Aerospace and higher revenue from tactical communications equipment and arresting systems. For the full year, the company reported an 11% increase in sales to $2.8 billion, due to strong performance in the Defense Electronics segment, driven by higher contributions from the arresting systems business, a healthy backlog, and easing supply chain issues.

Curtiss Wright operates through three reportable segments, namely Aerospace & Industrial, Defense Electronics, and Naval & Power. So, to better understand the company’s performance, we will discuss the results by segment in detail.

The Aerospace & Industrial segment’s revenue for the quarter increased by 6.7% YoY to $238.2 million, driven by strong double-digit growth in Commercial Aerospace OEM sales, partially offset by the timing of actuation development in the Defense market and a flat General Industrial market. For the full year, its revenue increased by 6% to $887.2 million, due to the strong Commercial Aerospace market.

The Defense Electronics segment’s revenue in Q4 increased 1.4% YoY to $239.8 million, driven by growth in the Ground Defense and Naval Defense markets due to higher revenue from tactical communications equipment. This was partially offset by the timing of sales of embedded computing equipment in the Aerospace Defense market. This increase was on top of record sales in Q4 2022. For the full year, it increased by 18% to $815.9 million, led by strong growth in the Defense market.

The Naval & Power segment’s revenue in Q4 increased by 3.3% YoY to $307.8 million, driven by strong global demand for arresting systems equipment, partially offset by a flat Naval Defense market, as higher revenue from Colombia class and Virginia class submarine programs were countered by decreased revenue from aircraft carrier programs. Additionally, growth for the Power & Process market was strong due to industrial valve sales, but it was offset by low China direct AP1000 program revenue. For the full year, it increased by 11% to $1.14 billion, driven by solid demand for arresting systems equipment and higher growth for Naval Defense.

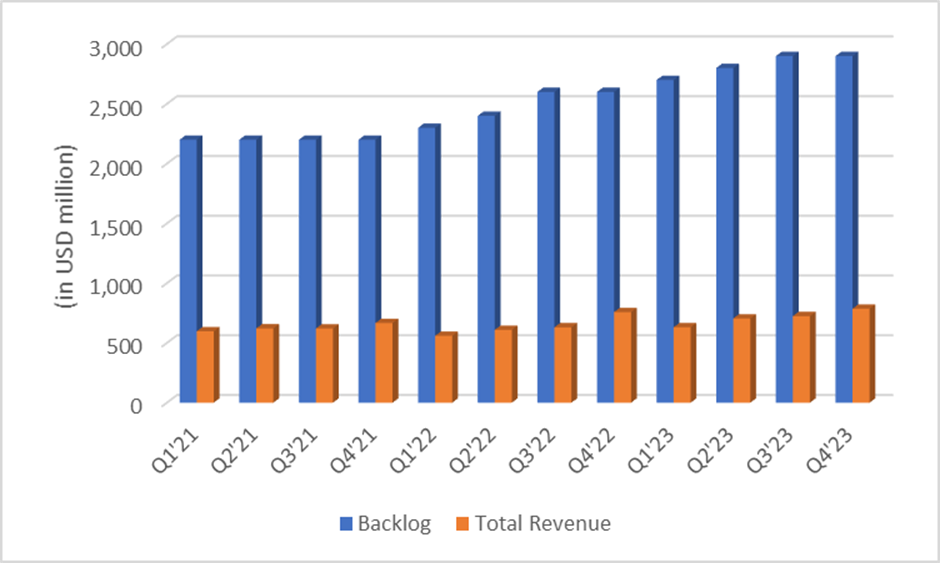

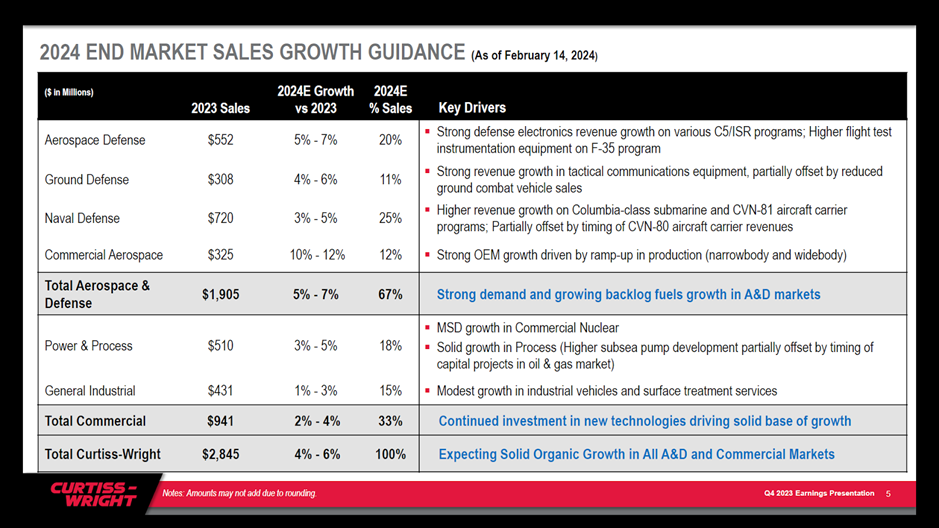

Looking forward, I am positive about the company’s near-term outlook. CW’s new orders for the full year increased by 5% to $3.1 billion, with an overall book-to-bill ratio of 1.1x. Its reported backlog of $2.9 billion increased by 9% YoY at the end of the fourth quarter. This was because of strong demand in both Aerospace Defense and Commercial end markets and provides the company with a good opportunity if they can successfully convert backlog into revenue.

The long-term outlook for the company also appears positive. Curtiss-Wright’s strategic acquisition of Arresting systems in June 2022, a designer, and manufacturer of fixed-wing aircraft emergency arresting systems, has been seeing robust demand globally, and I expect the strong momentum for the asserting system to continue benefiting the company in the long term. The company is also well-positioned to benefit from growing demand for nuclear energy in regions like China, India, and Eastern Europe with its differentiating products like coolant pumps for Westinghouse AP1000 reactor design and critical systems for X-energy’s Generation IV Xe-100 advanced Small Modular Reactor (SMR).

Furthermore, the company should also benefit from the new upward trend in defense spending worldwide, including the U.S Department of Defense’s increased budget. Overall, with strong demand for Curtiss Wright’s products and improving supply chain issues, I am positive about the long-term outlook for the company’s top-line growth.

Profitability Analysis And Outlook

Curtiss-Wright’s adjusted operating margin for the full year improved by 10 bps YoY to 17.4%, and for 4Q 2023, it decreased marginally by 30 basis points YoY to 20.8%, as overhead absorption on higher revenues was balanced by an unfavorable product mix and increased investments in R&D. Operating margin across the segments remained under pressure in Q4 2023 compared to the prior quarter last year. For the Aerospace & Industrial segment, it remained flat at 18.5%, for Defense Electronics, it decreased by 90 bps to 28.8%, and for the Naval and Power segment, it decreased by 100 bps to 19.3%, due to an unfavorable product mix and timing of development contracts for advanced SMR and subsea pumps. For the full year, operating margin improved by 110 bps for Defense Electronics, while it decreased by 10 bps and 120 bps for Aerospace & Industrial and Naval & Power, respectively.

In Q4 2023, the company’s adjusted diluted EPS of $3.16 beat consensus estimates by $0.24, and for the full year 2023, it was $9.38, an increase of 15.4% YoY, driven by strong top-line growth, improving operational performance, and share repurchase of $50 million. The company has consistently been able to generate double-digit growth in full-year diluted EPS, and since investor day 2021, it grew by around 12.5% CAGR. Therefore, I believe the management should be able to achieve its guidance of mid-single-digit growth for next year as well.

Looking forward, I expect the company’s profitability to be somewhat mixed in the near term as benefits from the absorption of higher revenue should be offset by some near term downward impact due to increased R&D investments and timing of development contracts for ASMR and subsea pumps. However, these strategic investments in research and development in the long run should benefit the company with strong organic growth.

Valuation

Curtiss-Wright currently pays a dividend of $0.80 annualized or $0.20 quarterly, with a forward yield of 0.34%. Even though the company has increased its dividend payment marginally in the last eight years, this is still low compared to its 5-year historical forward dividend yield of 0.53%. With a payout ratio of only 8.4%, there is enough potential for a dividend increase in the future. The company is more active with share repurchase programs as they believe share repurchase is the most effective method to drive shareholders return. As a result, it has repurchased shares worth $1.05 billion in the last eight years while reducing the share count by 9.2 million shares, and I expect the company should continue to repurchase shares in the future as well but at a slower pace as we have witnessed recently.

In another method, I am using the forward P/E ratio of Curtiss Wright to compare it with the industry average forward P/E ratio of around 20x to 25x. Using the middle multiple from that range, i.e., 22.5x, and based upon FY24 consensus EPS estimate of $10.23, the value of the CW stock comes around $230.17. I believe at a CMP of ~237.59, it is fairly priced, and to buy this stock I would wait for some correction or an exceptional financial performance by the company in the upcoming quarters.

Conclusion

In Conclusion, Curtiss-Wright is currently fairly valued, and I believe it already reflects the company’s recent performance and growth trends. Therefore, unless there is substantial improvement in its dividend yield or its financial performance, I would only suggest holding your existing position. Due to those positive factors discussed earlier being offset by its current valuation, I have a hold rating on CW stock at current levels.

Subscribe to receive future updates before anyone else.

Disclosure

This article contains author(s) opinions. The author of this report is not a licensed broker, research analyst or investment advisor. Therefore, It should not be taken as investment advice or recommendation.

The author of this report, or a member of their household, does not hold a financial interest in the securities of this company, and is not aware of any conflicts of interest that might bias the content of this report.

Hi to every body, it’s my first go to see of this website;

this weblog includes remarkable and truly excellent information for visitors.