Summary

- Primoris Services Corporation’s revenue growth is expected to benefit from a solid backlog and improved backlog-to-sales conversion.

- The company’s Energy segment is poised for strong demand in renewables and industrial markets.

- Primoris has a strong liquidity position and aims to reduce leverage further, positioning the company for future success.

- Primoris presents an attractive investment opportunity, trading at a discount compared to peers, with promising growth prospects in the construction and engineering industry.

Thesis

This article provides a detailed analysis of Primoris Services Corporation (NYSE: PRIM), focusing on its recent financial performance, growth prospects, and key strategic initiatives. Through an examination of its financial reports, earnings call, and guidance, this article aims to offer investors a comprehensive understanding of PRIM’s business model, competitive advantages, and potential risks. By highlighting its solid revenue growth, backlog strength, strategic focus on margin improvement, and strong liquidity position, this article seeks to test this thesis, and answering in detail why Primoris is an attractive investment opportunity in the construction and engineering industry.

Introduction:

Primoris Services Corporation is a leading provider of construction, infrastructure, and maintenance services, serving diverse industries such as energy, utilities, and telecommunications. Founded in 1946, the company has established a strong reputation for delivering high-quality projects on time and within budget. With operations spanning across the United States and Canada, Primoris has built a robust portfolio of clients and projects.

Why Primoris?

There are many reasons as to why anyone should consider investing in a stock which has already given around 65% returns in the last one year, but I will discuss few important ones in this article. Primoris’s recent financial performance reflects its resilience and adaptability in challenging market conditions. In its latest 10-K filing and quarterly update, the company reported solid revenue growth, driven by strong performances in its Energy segment. Additionally, Primoris’s strategic focus on margin improvement and cost optimization initiatives has contributed to its overall financial strength and stability.

Primoris stands out in the construction and infrastructure sector due to several key differentiating factors. Firstly, the company’s diversified business model allows it to capitalize on opportunities across multiple sectors, mitigating risks associated with industry fluctuations. Secondly, Primoris’s strategic expansion into high-growth markets such as renewables and telecommunications position it for long-term success and sustainability. Lastly, Primoris’s commitment to operational excellence, safety, and innovation sets it apart from its competitors, earning the trust and loyalty of its clients.

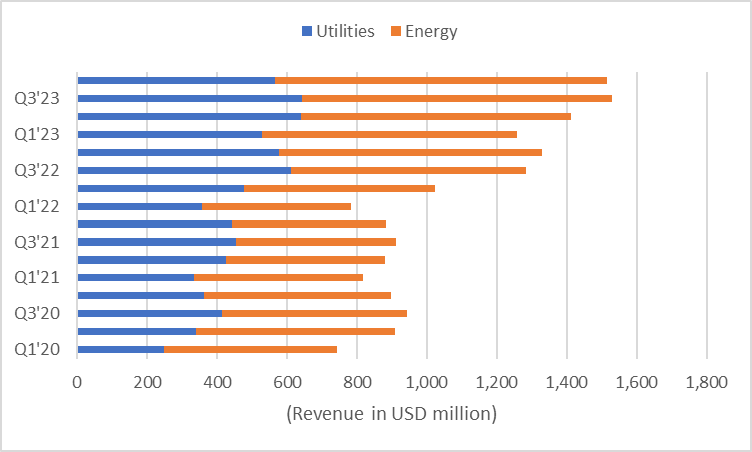

Solid Revenue Growth and Backlog Strength

Primoris has consistently delivered strong revenue growth, driven by its Energy segment’s solid performance in renewables and industrial markets. In its most recent quarterly report, the company reported a 14% increase in revenue compared to the prior year, reaching $1.5 billion. The Energy segment, in particular, saw significant growth, fueled by demand for renewables and increased industrial activity.

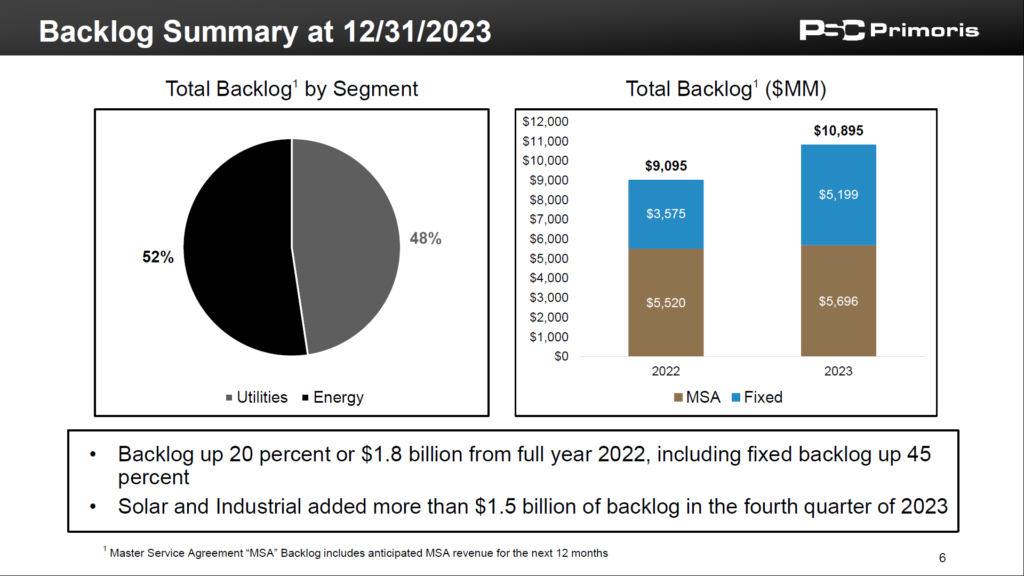

The backlog has been increasing consistently for the last few years, and it ended the year with record high total backlog of approximately $10.9 billion primarily due to strength in the Energy segment from renewables, particularly solar, heavy civil and industrial demand, and multi-year project wins. This gives a good opportunity for the company if they can convert backlog into revenue successfully.

Renewables and Industrial Markets Driving Growth:

Primoris’s Energy segment continues to be a key driver of revenue growth, with strong demand in renewables and industrial markets. The company’s strategic focus on solar projects and heavy civil construction has yielded positive results, with recent awards totaling over $1.1 billion in utility-scale solar and natural gas repowering projects.

Challenges and Opportunities in Utilities Segment:

While Primoris’s Utilities segment faced some challenges, particularly in gas utilities due to declining customer spending, the company is actively addressing these issues. The power delivery business experienced double-digit growth, offsetting the impact of lower volumes in gas utilities. Moreover, margin improvements are expected following the completion of low-margin projects, providing a balanced outlook for the Utilities segment.

Looking ahead, I am optimistic about its growth prospects. I anticipates continued revenue growth for the company, supported by a strong backlog and favorable industry trends. Robust demand for renewables, driven by solar projects and communications infrastructure, along with contributions from the Inflation Reduction Act (IRA), are expected to fuel Primoris’s growth in the long term.

Strategic Focus on Margin Improvement

Primoris has implemented effective margin improvement strategies to navigate through market challenges and enhance profitability. In Q4 2023, the company’s gross profit improved slightly to approximately $157 million, with gross margins declining to 10.3% primarily due to lower margins in the Utilities segment. Despite this, Primoris remains focused on margin enhancement initiatives, particularly in the Utilities segment, where efforts to address legacy project costs and negotiate market-rate contracts are underway.

In the Energy segment, gross profit increased by over 36% to $114 million, with gross margins improving to 12% compared to the previous year. This improvement can be attributed to the growth in renewables business and improved industrial margins. Primoris anticipates further margin expansion in the Energy segment driven by ongoing tailwinds in renewables and industrial markets, coupled with the integration benefits from recent acquisitions.

The company’s SG&A expenses witnessed a decline in Q4 2023, contributing to improved adjusted EBITDA margins. Primoris remains committed to optimizing its cost structure and expects further margin improvements in the near term. Efforts to renegotiate base rates, adjust costs, and optimize project mix are expected to drive margin improvement, particularly in the Utilities segment. Additionally, the integration of PLH and declining SG&A expenses contribute positively to margin expansion, further strengthening Primoris’s financial position.

Leverage Reduction and Strong Liquidity

Primoris ended Q4 2023 with a strong liquidity position, with cash reserves of $160.7 million and borrowing capacity of approximately $273 million under its revolver. The company made significant progress in deleveraging, with net debt decreasing to approximately $747 million, positioning it well to achieve its leverage reduction targets. Operating cash flows for the quarter were approximately $206 million, reflecting improved working capital management and early customer payments.

Looking ahead, Primoris aims to further strengthen its balance sheet and liquidity position, enabling it to pursue strategic growth initiatives and capitalize on emerging opportunities in the construction and infrastructure sectors.

Valuation

Primoris has appreciated by around 65% in the last one year, but if if see the bigger picture, the company has remained flat for almost a dacade up untill this strong rally which began by late 2022. This rally started with the phenomenal results PRIM posted in the third quarter of 2022, when both its revenue and profitability improved, and since then the revenues is growing in strong double digits. So I believe its current price is completely justifible, and I further see big upside potential in the stock.

By Relative valuation, Primoris is currently trading at 13.88x FY24 consensus EPS estimate of $2.84 and 12.07x FY25 consensus EPS estimate of $3.27. This is a discount of approximately 35% compared to the sector median of 18.85x. The company also has a low forward PEG ratio of 1.03 compared to the sector average of 1.77. I have also used EV/Sales ratio to accurately reflect the company’s value for its presence in high-growth industries. Its forward EV/Sales ratio is 0.55, which is low compared to sector median of 1.8. Therefore, the company appears to be undervalued compared to its peers, and I expect these valuation metrics to improve in the forthcoming quarters.

Risks to Consider

While Primoris presents an attractive investment opportunity, investors should remain mindful of potential risks inherent in the construction and infrastructure industry. Market volatility, regulatory changes, and macroeconomic headwinds could pose challenges to Primoris’s growth trajectory and financial performance. Moreover, operational risks such as project delays, supply chain disruptions, and cost overruns warrant careful consideration. Geopolitical tensions, environmental regulations, and labor market dynamics further underscore the need for prudent risk management. Investors should conduct thorough due diligence and assess these risks before making investment decisions in Primoris.

Conclusion

Primoris Services is currently trading at a discount compared to its peers. In my opinion, the stock is not reflecting its growth potential correctly, which is expected to remain robust, based on my thesis, as a result, I anticipate strong upside potential in the stock price. The company may face some near-term challenges if it is unable to bring down its leverage ratio as planned, causing hindrance to further acquisitions and expansion prospects, but seeing recent progress the company has made, I expect it should be able to achieve it. In conclusion, we have discussed how various factors such as a solid backlog, strategic acquisition, and improving leverage ratio coupled with industry trends should support the long-term revenue growth of the company. Therefore, I have a buy rating on PRIM at current levels.

Subscribe to receive future updates before anyone else.

Disclosure

This article contains author(s) opinions. The author of this report is not a licensed broker, research analyst or investment advisor. Therefore, It should not be taken as investment advice or recommendation.

The opinions shared in here are only for educational purpose and should not be taken as recommedation to Buy/Sell/Hold any kind of securities.

The author of this report, or a member of their household, does not hold a financial interest in the securities of this company, and is not aware of any conflicts of interest that might bias the content of this report.

Keep posting